SK Telecom $SKM Handing Out Free Stakes in $2T Anthropic

Don't take that sentence too literally, but it is factually correct if you believe my analysis below.

UPDATE 1st June:

I finessed the methodology (totally left out HoldCo discount for investments...).

$SKM price down as of 29 May close (before today’s 10% upwards riot).

Listed investments (PENG and IONQ especially) went up.

$65B funding ($50B new) at $965B post-money. Dilution of $SKM stake duly plugged in.

25% HoldCo discount added to all $SKM investments.

The world isn’t ready for Anthropic at $4T. I’ve put $2T in the SOTP this time. Because who are you kidding, this is the reason to buy the stock.

Model here.

Also, OpenRouter data has Anthropic dominating even more.

New SOTP

TLDR

• I mistook Claude for being French for quite some time.

• Anthropic is vastly under-valued, mainly because bigger numbers are intimidating.

• Real time alternative data indicates the market may be under-estimating Anthropic’s dominance.

• Using that data, market commentary and comps, I argue Anthropic is worth $4 trillion today.

• A listed early investor in Anthropic, SKM 0.00%↑ has all kinds of other jewels in its portfolio buried deep in the Korean regulatory disclosures.

• The riddle of their ownership stake in Anthropic is clarified.

• With a little hyperbole, I reveal this amounts to a back door to investing in Anthropic, in the public markets, for free.

• The Anthropic proxy has 150% upside with a SOTP valuation.

• I am not a qualified financial analyst, though know a thing or two. Not Financial Advice.

• I could not really explain what a semiconductor is. DYOR.

You can see the more detailed and less flippant model that underpins this analysis here.

Part 1: The $4 trillion Anthropic

No business ever has, or likely ever will, be like Anthropic. I am going to explain why the market is colossally underpricing them at a mere trillion.

I had been using Claude alongside the other big dogs for a while, and of course it was nice to see a European company up there, even if it looked a little off the pace next to Googs and OpenAI. However it always wrote more fluently. I put it down to the usually insufferable Gallic habit of being extremely well read.

I digress. Let us get into some technical analysis of how Claude managed to sneak up from behind (classic French move ofc).

Well Claude just went ballistic.

Tech analysis over.

They started shipping updates at a speed that seemed impossible.

Actually turns out the French are cheating again. The devils are using their AI to build new AI! That’s not cricket if you ask me.

Yet his tools were astonishing. There is nothing like a Frenchman in his pomp. The stench of his monthly bathing schedule mixed with the aroma of fetid garlic was almost forgotten. He would build actual computer-y things (turns out a computer does more than internet-ing). Claude would smash out bangers over and over, and he would tut if I tried to press anything and interfere.

All those permissions definitely can have teething issues if you granted them too freely. Chum of mine got a bit trigger happy granting Claude carte blanche. The slimy frog stole his wife!

But now I barely notice he is foppishly wearing a scarf in the middle of summer, or smoking a Gauloise, as he churns out 50 hours of SWE time in 10 minutes. I have been Wispr-ing my prompts in a French accent to make his life easier.

That is the great problem we English suffer with having the French as our historical nemesis. Secretly, you can’t help but admire and envy them.

Well annoyingly Claude tricked me and turned out to be American also, but I still prompt in French regardless.

Let us get into it.

Revenue Explosion

Anthropic’s reported ARR by month:

YTD growth rate is 12,400% annualised. Holy smokes. Not even slowing down last month.

Last week Dario admitted Anthropic had “planned for 10x and saw 80x” growth in Q1. They have done incredibly well to hang on to their hats.

What The Growth Rate Implies For Year-End ARR

From the $45B April base:

Comparisons

The only company at this scale and growth rate to compare is NVIDIA, which peaked at 206% YoY in late 2023 at a $73B annualised quarterly run rate ($18B for the quarter). It became the world’s most valuable company a few months later. Today it sits near $5T on $200B revenue at 60% growth. EV / Revenue 24x.

Now the Newtonians amongst you will be jabbing their fingers about gravity. Gravity is real. Every company that flies out of the blocks spends the rest of its corporate life trying to arrest the declining rate of growth. Apparently it is a lot harder to add $10B of growth in a quarter than $10M.

The TAM Question

Gravity relates to TAM and capacity at the firm. Global enterprise IT spend, per finger-in-the-air merchants Gartner, is $1.6T. Capturing 20% market share by year end is impossible.

Lucky that is not the TAM. Knowledge work. Drug development. Medical devices. Gas exploration. Supply chains. Lawyers. Perfecting the baguettes of Paris (ofc not, that is the singularity definition).

Here is a sample of companies that have attributed firing 10% of their workforce to AI lately:

• Meta

• Dow Chemicals

• Citigroup

• Nestle

Now if you were a CEO and had over-hired, rather tempting to say you had made AI efficiencies (Nestle stock went up 9.5% upon announcement) rather than bluntly say “I am a moron” and get fired.

But the bloodletting is real and from the announcements, it is in every business.

I think TAM is titanic once you reframe your perspective:

• How important is it to implement fast everywhere in your org?

• Would you economise on the model if you thought your competitor was only using the best?

• Would you be yelling at the workers to spend more on AI to implement faster, or less and slower?

• Would you see this initiative as a project and ignore the rapid model advancements in subsequent months? Or would this implementation start fresh with every major update?

• Would spending 1% of your revenue to make seismic gains as the models accelerated seem worth paying for?

If I led you down the path just now, you can see how Claude could be trousering quite a few francs in the coming months and years.

The Competitive Moat

Now this thesis has rather presented Claude as a monopoly, which it is not, and that is a key hurdle to a higher valuation.

OpenAI’s new drop is supposedly just as good or better. Google are no doubt up to something too. Then of course, what about all the other ones. Will buyers decide almost as good is good enough?

In FT-style prose, I have spoken with five people familiar with the matter. One of them actually knows what they are talking about, and they say “Claude first, the rest nowhere.”

This powerful market research is likely enough for most readers, but I have gone the extra mile.

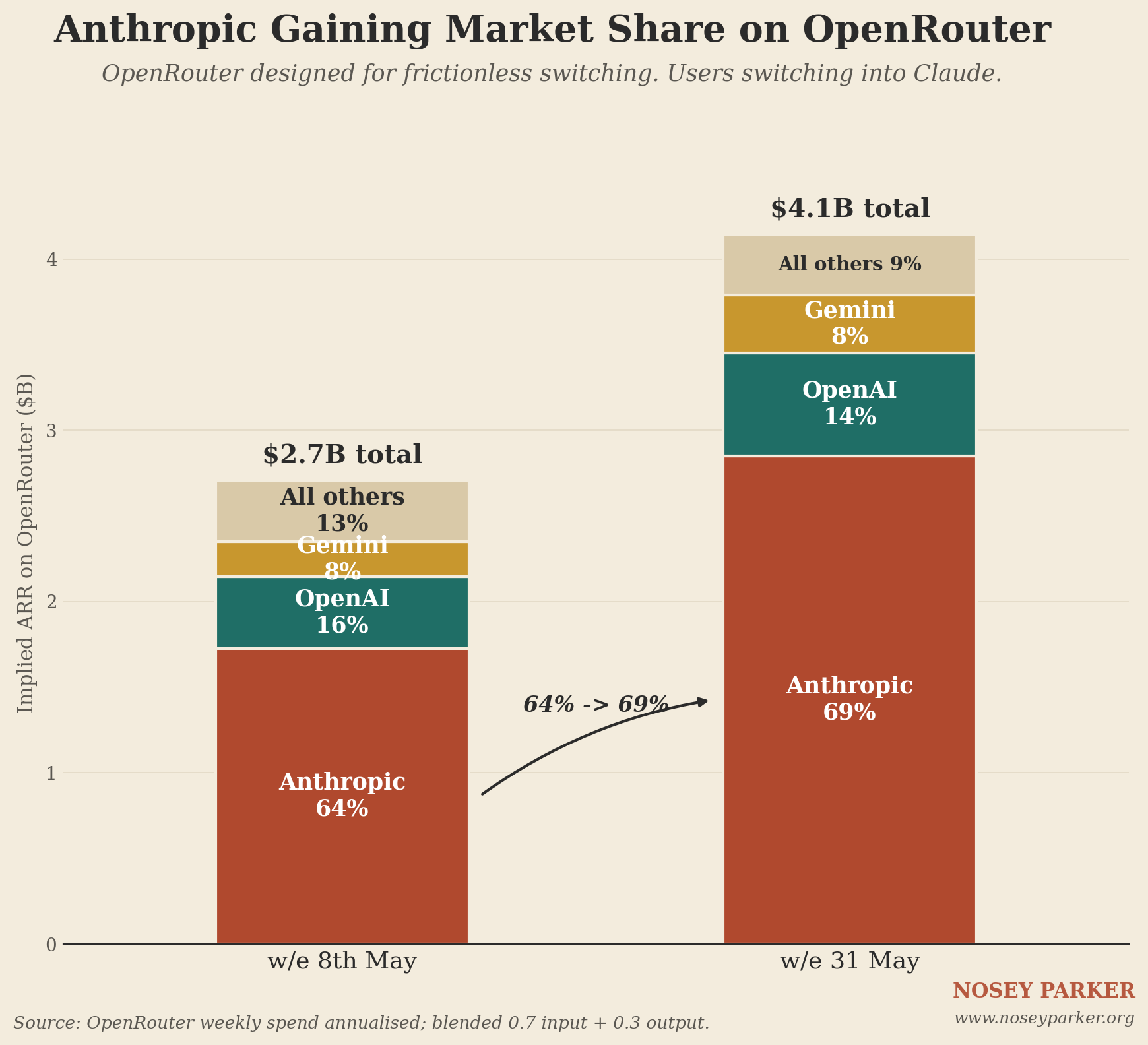

OpenRouter: A Rubbernecker’s Dream

OpenRouter is a website where you can register and switch between hundreds of models willy nilly. It is for the connoisseurs and the tinkerers. Little of that $45B is flowing through here, but it is a treasure trove just the same.

The data they share is up to the minute. You can see how all the models performed each day. The timeliness is glorious not only as a proxy for MoM growth. Claude spend grew on the platform by 50% last month. Same as the actual revenue.

Its potency is fantastic for seeing the enthusiasm and uptake of new iterations from all the players. Let’s see if 5.5 swept the floor in the end? Or are the almost-free options too hard to resist. Below see week ending Fri 8 May.

Good God. Anthropic taking 64% of the whole market. Charging double OpenAI and 8x Google. Moonshot can take a bow. Everyone else is nowhere. No wonder Musk was renting his Colossus out to Anthropic. 0.5% market share is a failed model if these are representative.

Note $33M for Anthro = $1.7B ARR. About 4% of the $45B. Not insignificant, but not definitive.

Like China in the Ping Pong at the Olympics. Gold, Silver, Bronze, the rest nowhere.

Things can change of course. But OpenAI has some demons within. Only two of the founding 11 members are still at the company. Three of the execs seemingly got ejected a couple of weeks ago. There is a vicious court case at the moment between Musk and Altman. There are demons in this company.

Anthropic, by comparison, have taken their ethical responsibility much more seriously. Indeed, the Anthropic founders came from OpenAI for this very reason. The speed of output and production on Anthropic seems like a hard gap for OpenAI to close. Google, of course, are a perennial competitor to take Anthropic’s crown, but boy, are they a long way away at the moment, as per that data.

Compute And The Value Chain

What about running out of compute? When there is a shortage of oil, how do the oil companies fare? Not a material threat.

What about users just being able to switch model at the drop of a hat, forcing prices into competition? That is very unlikely the way enterprise software is going to work. One would imagine that already multi-year contracts are being signed by a freshly minted enterprise sales team. God, they must be making some money.

The one obstacle to the bull case I’m presenting that I cannot comment on with any confidence is who is going to take all the money in this distribution chain. This industry is astonishing. Names are falling out of the sky that are cramming the top valuations in the world, and astonishingly, for very good reason. ASML sits at the top. They make the machines that make the machines. I don’t actually know what that means. But everyone seems to agree nobody else can. Apparently, you need 40 years of accumulated knowledge to get up to where they are, and presumably over those 40 years ASML will make some advances themselves.

Here are some words:

• Nano metres

• Width of a hydrogen atom

• Mirror that, if was the size of Germany, it would not deviate a millimetre.

• 100,000 independent widgets in just one machine

Like me, you don’t need to know what they mean. None of them relate to my three preferred reference points for size: packet of cigs, a football pitch, or the size of Wales. But they explain why ASML has zero competition. Nvidia and TSMC are not far away from their monopolistic position. The reason they have such strength can be summed up in the following sentence:

Everything in AI is really fiddly.

The other mesmerising valuations for Broadcom, SK Hynix, Intel, Samsung, Micron, and others all relate to the paucity of competitors.

There is a question about where all the profits will fall in that value chain. Compared to ASML, NVIDIA and TSMC, who face almost no credible competition for what they do, Anthropic sits in the most contested seat. OpenAI, Google and the long tail of open-source contenders are in the same arena. The OpenRouter data above tells you that Claude is winning on dollar share today, not that competition has gone away.

I can take faith in the dynamics of a natural shift towards customers demanding the best provider, and the users of that provider, like me, don’t even know why a mirror has to be the size of Germany (jk). They know they just need to mainline Claude. Thus Anthropic will maintain significant pricing power in the AI value chain.

DYOR.

Mythos

Claude has written a model, Mythos, that is too dangerous to release. Mozilla Firefox had it give their code the once-over. 271 vulnerabilities it found. Yikes. So the tech stacks of the world, and Mythos, need some polish before it can be released. However, it is in the hands of about 50 companies. JPM, Goldman and Morgan Stanley have it. Looks like many of their rivals don’t yet.

If I was Jamie Dimon, I would be passive-aggressively tapping my watch to ensure the workers got a wriggle on with this superpower. Not a time for fiscal restraint. Borrow some money. Fire some chumps. But get ahead.

Defending $4 Trillion Today

I go into the comps in the model, but the real comp for $45B annualised at this scale is NVIDIA a couple of years ago. They peaked at 206% YoY growth in Q3 calendar 2023 at $18B quarterly ($73B annualised run rate). Six months later, they knocked Microsoft and Apple off the perch and became the world’s most valuable company. Today, they are growing at 60% on $200B of revenue, 24x EV/Revenue, $5T enterprise value. Another reference point is Snowflake’s IPO, where they were growing at 121% and got 132x revenue. But that was at a paltry $500M of revenue. Palantir today on $7.7B of revenue, 85% growth, gets 42x EV/Revenue. For context the other way: Tesla today is at 12x revenue; revenue is shrinking 5% and they are worth around a trillion on $95B. Multiple is around 11x.

The comps are useless, but it has got to be higher, surely, because 12,400% is higher than 200%. Indeed, if they do not grow a single dollar in ARR for the rest of the year, they will still have grown 400% YoY. I am going to say 89x on $45B. I justify that a little more in the spreadsheet, but there is not a lot else to look at.

Multiples of revenue. Of course, acknowledging that some of these other companies were profitable by then, but profitability is almost irrelevant when you are going that fast. Gross margin is reportedly at 40% so the roadmap to profits is certainly there. They will never likely get to SaaS multiples, but from our comp set, none of them could ever dream of growth rates this fast at this scale.

The model walks through five independent methods.

* Forward Dec 2026 EV is discounted back to today by 1.12^(8/12) for the eight months between the May 2026 ADR price and the Dec 2026 forward ARR base. 12% is the assumed cost of equity. Per the model, Anth_Valuation tab.

I tried weighting different outcomes, which miraculously also got to 4 trillion. An unerring coincidence.

The model’s probability-weighted central:

$4T is the central, not the bull. For today.

The Bridge To Korea

However, it doesn’t matter a jot. Anthropic is a private company. I don’t suppose Claude will be rattling his tin too broadly if and when they raise again. $10B minimum cheque size might be on the low end.

Yet none of that gets in the way, because I am going to tell you how you can invest in Monsieur Claude. Minimum ticket size $1. No max. The $10B+ investors are going in at $1T minimum valuation.

What Anthropic’s valuation actually is matters less than you think, because I am going to show you how to acquire a stake in Anthropic for free.

The most intelligent of you will instantly see this is the opportunity of a lifetime, take my word for it, and want directions to the cash volcano. The simpletons alas will have their customary scepticism that I will be forced to address.

Every word above is based upon the truth, but I must admit I have used words that may give the wrong impression.

For now I must say au revoir to Monsieur Claude. The absolute frontier of human development will take an unlikely path to a chaebol in Korea. I worked as a salaryman for their more illustrious rival in Gangnam for a year or two. What chance that it will help me be your jungle guide 20 years on.

Part 2: The Schleswig-Holstein question

“Only three people have ever really understood the Schleswig-Holstein business. The Prince Consort, who is dead. A German professor, who has gone mad. And I, who have forgotten all about it.”

The ownership structure of Samsung is almost the same. Nobody was ever able to explain how it all worked. Just one thing was known with certainty, and that was all the actual power of the conglomerate was in Samsung Everland. An owner of a theme park that proudly boasts as their tagline on their site: “the drier park ... of two famed parks.”

I’ve never looked this up since because if I look it up, it might then know it is not true. I prefer believing what I was told.

I only say this so you now understand I do have some experience of Korean chaebol. But only a little.

I am taking you to the SK Group, who were rather the dullards compared to LG and Hyundai when I was there, but now they managed to make one of the fiddly bits in the AI production chain (SK Hynix jumped from $100B to $1T in the last year). Not to that subsidiary. To a much more unlikely place than you could imagine: SK Telecom, the Korean version of Verizon.

SK Telecom is a mature mobile operator and broadband provider serving South Korea. Revenue roughly $12.5B. Not glamorous.

The Headline Numbers

Telco businesses are really boring, normally. Hard to grow when:

• Wi-Fi and 5G are fast enough.

• Nobody wants a landline.

• Cable TV’s in decline.

You can only really make more money by:

• Duping your punters into an upsell they don’t really want

• Squeezing 50 basis points on cost

Capex is largely done, so good cash flows but not going anywhere. A quasi-utility.

SKM even bungled that. They had a data leak, and it was quite bad. Quite a few customers left, and they were pretty annoyed. There’s a hangover from that, not in terms of financial fines but a poor reputation. It seems to have turned the corner, and subscribers are growing again. This is reflected in the revenue and profit. If you look at the consolidated financial statements, they are not great. The data leak cost a bunch of money to remediate.

SK Telecom’s AI Pivot

In 2022 SKT made a song and dance about becoming an AI company. This was, at the time, somewhat laughable. Hard to think of a claim to being a tech company that is more tenuous than “we do broadband.” They pressed on anyway and made a series of investments. From the cash flows of the core business, they started spending money like sailors in port on all kinds of crackpot investments. If it had AI in it, they invested. This was to the discredit of management in the markets until recently. The CEO behind this was subsequently fired.

There has been almost no coverage that I’ve found of this investment portfolio. That makes sense. The only place I found it disclosed was in the business report, which is a separate document in Korean, not in the English version (16 pages) but in the Korean-language version (nearly 500 pages).

Those who may read this and knew me in Korea will probably know only one thing about me: I was the most gifted Korean language student they had ever seen for dense business and technical terms. It was my passion, my reason to exist. They laughed. What a waste of time it was. They don’t laugh today.

Actually, I never learned a word of Korean, and my good man Claude found what I was looking for in about four seconds on pages 441 and 442. Turns out investing in AI in 2022 had some merit.

The Investments That Matter

You can see the line-by-line in the spreadsheet, but it turns out this artificial intelligence was not a flash in the pan. Let me run you through the highlights.

Minority investment accounting was never my sweet spot, and it’s quite dense. Just ‘trust me bro’, and don’t actually take my readings as gospel, but they should be good.

In this list there are different types:

• Mark-to-market, where the entity is listed, so you can update that number in a moment

• Equity accounting, which is notoriously unrepresentative of value

• Fair value accounting, which is a bit of a mess, but should be the auditor’s agreed assessment of the correct value at year end. This invariably applies a DLOM of 25%.

I updated the mark-to-market valuations in the list, and some have shown extraordinary equity growth. For others, I reviewed the AI holdings that, based on public information, may warrant a revaluation.

Here are the six positions worth a line each. Anthropic excluded; that is the next section.

Details of the other smaller investments and their uplift are in the model. Listed investments have been updated with the current share price. Here are a few details on the non-listed investments:

Rebellions. Korean AI silicon designer. Pre-IPO priced round in March 2026 had it at $2.3B.

Persona Identities. SKM holds 3.9%. Last priced round was $2B in April 2025. I have marked Persona at $3.5B, a value judgement based on commercial performance and secular trends since the last funding round over a year ago. The fuller justification (Anthropic vendor selection, LinkedIn and Reddit logos, headcount doubling, regulatory tailwinds, comparable transactions) is set out in the model.

Perplexity AI. AI search. SKM put $10M in during June 2024. Implied $25B secondary. 0.33% stake. Marked at $62M after 25% DLOM. 6.2x money in less than two years. The market value depends on whether Perplexity actually has a defensible business or whether it ends up as a feature on someone else’s chatbot. But the priced rounds keep printing higher.

All together, the revaluation gives the investment portfolio a mark of $3.9B against a book of $2.1B, an uplift of $1.8B over what the accounts alone would have you believe.

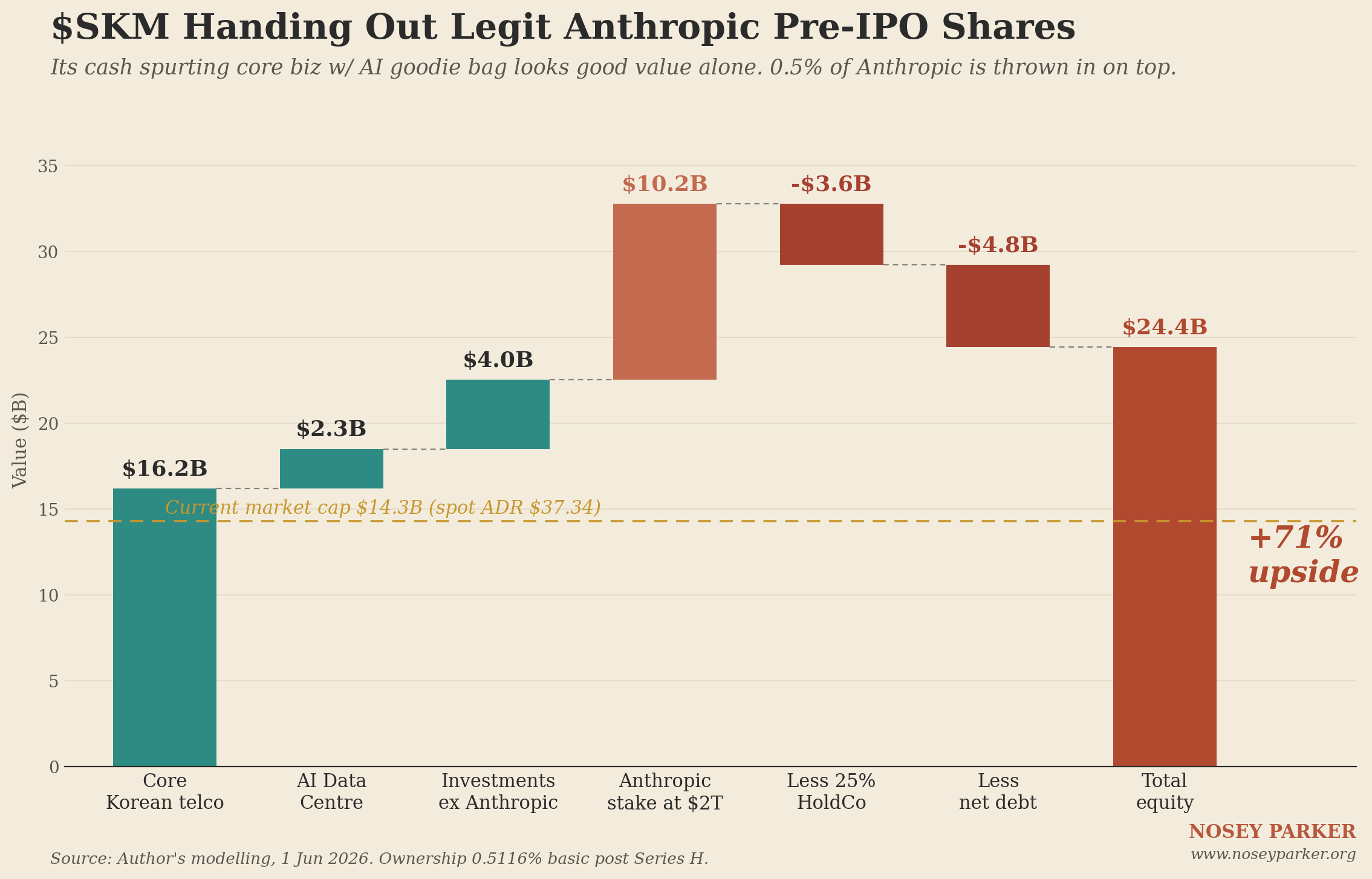

The Core Business

A mature Korean telco at 81% 5G handset penetration deserves a pedestrian multiple. Wireless capex fell 42% in FY2025. The 5G build is done. D&A continues to charge the income statement above maintenance capex, which means the cash generation is understated. AI Data Centre revenue in Q1 2026 was $89M quarterly, up 28.8% YoY but down 17.6% QoQ from the Q4 2025 Pangyo step-up. Annualised that is $356M of run rate on the operational footprint of Gasan and Pangyo, which now sits at its capacity ceiling. KEPCO power-connection lead times of 12+ months and MOTIE’s metro-build restrictions mean SKM’s existing operational MW are scarce assets in the highest-demand AI training market in Asia. The capacity-bound dynamic supports the $2.3B SOTP mark; new capacity from the announced FY26 Seoul-metro build will not contribute revenue until 2028.

I value the core at 4.5x Korean peer median EV/EBITDA, which gives $16.2B. The DCF on the same business gives c. $20B; I use it as a sense-check rather than the central, because for a mature Korean telco the comp set has more gravity than a single-firm five-year DCF.

Sum Of The Parts

SKM appears to be trading at a 15% discount to a defensible sum-of-the-parts. A Korean telco with a nice AI portfolio at a discount.

Korean Sell-Side Coverage

Korean sell-side coverage is split. Spot ADR is $39.08 for reference.

Telco equity analysts do not think in revenue multiples. They think in cash flow forecasts and have not looked at SKM in the right manner. No better example is Goldman Sachs, who in their Q1 2026 report reiterating their sell opinion and do not once mention any of the investments made and give no attribution to them in their model.

Worth noting that the historical Korean discount on holding-company structures has been narrowing materially. The Commercial Code Amendment that came into force on 22 July 2025 extended directors’ fiduciary duty explicitly to shareholders, not just the company. President Lee Jae Myung’s Value-Up programme is the first serious legislative attack on the chaebol governance regime that produced the discount. The KOSPI is up roughly 80% year-to-date 2026. The “30-50% NASPERS-style discount” base case assumed in older SOTP work on Korean holdcos is anchored to a regime that is being actively dismantled. SKM benefits structurally regardless of the Anthropic outcome.

That is the SK Telecom story. A telecom company, a set of investments worth meaningfully more than their book values, and a 15% discount to intrinsic value.

Part 3: About that other investment

Oh. One more thing.

The sum-of-the-parts valuation of SK Telecom more than justifies its current valuation. However, I left one of their investments aside.

In August 2023, SK Telecom invested $100M in Anthropic and acquired (their language at the time) a “2%” stake. Anthropic was being priced at around $5B at the time.

This is what you get for free on top, if you buy shares in SK Telecom.

Since the investment, Anthropic has raised quite a lot of capital.

The ownership question is where this gets interesting, and where almost every analyst who has touched it has gone wrong.

The market consensus puts SKM’s Anthropic stake at approximately 0.30% on a fully diluted basis. This figure is cited in English-language press, picked up from a loosely worded SKM disclosure, and propagated without verification.

It is wrong, and the error is in the denominator.

The Correct Chain

Page 441 to 442 of the 2025 Business Report (Korean edition, 442 pages, not the 16-page English summary) discloses 3,703,141 shares at a 0.7% stake as of year-end 2024 (opening balance for FY25), with a carrying value of $132M at the disclosure FX rate.

Korea Investment & Securities analyst Kim Jung-chan stated in January 2026 that SKM held 0.7% of Anthropic per the H1 2025 semi-annual DART filing. He is a covered analyst at a tier-one Korean broker quoting a primary regulatory filing.

PitchBook reports 1.47B fully diluted Anthropic shares. That figure includes authorised-but-unissued option pools that have never been granted. Those do not dilute SKM economically.

The treasury stock method, mandatory for public-company diluted EPS, only counts options to the extent they are in the money and net of strike. Reserved-but-ungranted pools are excluded.

Anthropic’s auditor Samil PwC switched from basic to fully-diluted presentation between the H1 and FY 2025 disclosures. The economic reality, the share count, did not change. The disclosure convention did.

Working Forward To Today

Starting from 0.7% basic at H1 2025, threading through:

• Series F (September 2025), $13B raised at $183B post-money, approximately 7% dilution

• Series G (February 2026), $30B raised at $380B post-money, approximately 8% dilution

• Employee tender offer (February 2026), conversion of vested options

• Amazon $5B at $350B pre-money (20 April 2026), approximately 1.4% dilution

• Google $10B at $350B pre-money (24 April 2026), approximately 2.8% dilution

SKM’s basic ownership at 13 May 2026 is 0.54%.

Korean sell-side at Meritz Securities and Korea Investment & Securities both cite approximately 0.58% post-Series-G (pre April 2026 strategic equity). That corroborates the calculation within rounding. Any reader can trace this themselves in the filings. The 0.30% figure being used by the market is the wrong denominator on the wrong share count.

Google is contractually capped at 15% of Anthropic, with no voting rights and no board seat. So further dilution from this counterparty is structurally limited.

What 0.54% Of Anthropic Is Worth

Applying a 5% illiquidity discount (compressed from the standard 25% K-IFRS Level 3 given IPO expected within 6 to 9 months):

Carrying value on the SKM balance sheet today is $962M (auditor-declared, no methodology disclosed). Cost was $100M. Already 9.6x on book without any forward mark.

The Implied Anthropic Valuation At The Current SKM Price

At central marks for every other asset, SKM’s ex Anthropic equity comes to $17.7B against a current market capitalisation of $15.0B. The premium of ex Anthropic equity over market cap is $2.7B, or 18%.

At the current price, the market is giving you the Anthropic stake for free. Or better than free.

Only at core EV/EBITDA multiples below the Korean peer median does the market start to credit any Anthropic value at all. At the actual Korean peer median multiple of 4.5x, the market prices Anthropic at less than zero. The deal-of-the-century framing is not hyperbole. It is arithmetic.

The Full Picture

Total SKM equity at various Anthropic outcomes, with the implied ADR price at each:

At every Anthropic valuation at or above the priced Series G, SKM is cheap. The only scenario in which it is not cheap is one in which Anthropic is overvalued at $380B. You are welcome to take that view. It requires believing that a company doing $45B ARR, growing 5x YTD, with Jamie Dimon on stage, ten gigawatts of committed compute, and a cybersecurity model the White House has cleared for federal use, is worth less than $380B. Good luck.

Claude is still wearing that foppish scarf and it is mid-May on the Mediterranean. I forgive him.

You can see the more detailed and less flippant model that underpins this analysis here.

Risks

The SK Telecom business risks are largely irrelevant given the entire upside thesis sits on Anthropic. The risks to my $4 trillion Anthropic valuation are laid out previously.

It is worth noting the additional risks of the proxy in between, the Korean holding company. Such structures have historically traded at a discount due to the opaque governance often involved, where the interests of the owners are not always aligned with the interests of the shareholders. Though this is not exclusive to Korea, investors in NASPERS and their titanic success in investing in Tencent have pulled their hair out, as much of the proceeds remain within NASPERS, which has continued to incinerate shareholder value in other investments rather than return the money. That risk is real. Yet the NASPERS comparison is perhaps unfair, as firstly, SKM is not run by a lunatic, and secondly the other investments shown by SK Telecom have also performed extremely well; but the transmission of the proceeds of an Anthropic IPO to shareholders should not be ignored.

The other main risk is the opacity of the ownership stake in Anthropic. It is far from clear through the company’s own communications, and the most compelling evidence is buried deep within Korean-language reports. The value ascribed in this analysis could be off by 20%, and shareholders are unlikely to receive much clarity going forward. Not only through cautious disclosures from SK Telecom but also Anthropic’s insistence that shareholders do not share proprietary data.

Catalysts

Four catalysts for price discovery over the next 6 to 9 months. The first three are information events that should help clarify the thesis. Only the fourth, the IPO, provides full mark-to-market resolution.

1. May ARR print (expected mid-June). $50 to 60B confirms trajectory. $65B+ validates the central case as conservative. Anything below $50B requires reweighting the probability distribution and compressing the central from $4T to $1.5 to 2T.

2. Mythos broader release. Currently restricted to JPM, Goldman, and a small set of partners. Treasury and Fed engagement is active. A broader rollout, with announced enterprise contracts at scale, repositions Anthropic from frontier AI lab to systemically important infrastructure. The Mozilla disclosure (271 vulnerabilities surfaced in Firefox in a single day) is the technical proof-point already in the public domain.

3. Series H pricing. Bloomberg and TechCrunch have the active round in the $850 to 900B range and imminent. The pricing sets the floor for IPO discussion. A close above $900B collapses any remaining argument that Anthropic at trillion-plus is speculative.

4. IPO. Goldman, JPM and Morgan Stanley are named as underwriters. Wilson Sonsini S-1 filing rumoured Q3. Target window Q4 2026 with October the earliest. On IPO the K-IFRS Level 3 illiquidity discount collapses to zero and the SKM stake becomes a mark-to-market liquid public security overnight. That is the one event that resolves the thesis.

This document is an independent investment analysis prepared for personal use. It does not constitute investment advice or a recommendation to buy or sell any security. The author is not a registered investment advisor. All sources are publicly available. Conduct your own research.

Woah wtf? This post is waaaay underrated, amazing job! was looking for DD on SKM because I thought anthropic was mogging everyone else, did not disappoint my friend :)